Are AI Companies Really Overspending?

Markets may be entering a familiar two-stage behavior pattern: first, pressure from heavy investment and uncertain payback; later, relief when capital discipline becomes credible.

For a year, I kept seeing one claim:

AI companies overspend on CapEx.

I wanted one concrete answer. Are companies actually becoming more disciplined with capital allocation?

I skipped the debate, pulled quarterly numbers from public filings, built a dataset for the largest AI infrastructure names, and checked the evidence.

I define overspending in plain terms:

CapEx grows faster than internally generated cash long enough for the gap to keep widening.

Methodology

Why these companies?

I picked the companies that drive infrastructure spend and move the narrative:

- AAPL

- AMZN

- GOOGL

- META

- MSFT

I kept NVDA and ORCL for context. I read the regime through Big 5 and ex-AAPL.

Why these metrics?

I tracked three metrics:

- CapEx: the scale of infrastructure investment.

- FCF: the cash left after investment.

- CapEx/FCF: a direct pressure indicator.

When CapEx/FCF rises, management pushes a larger share of cash generation back into infrastructure.

Why rolling LTM?

Single quarters swing on seasonality and one-offs. Rolling LTM filters that noise and shows direction.

I tracked Q-9 to Q0 with two lenses:

- Big 5 aggregate.

- Ex-AAPL AI-heavy aggregate (AMZN, GOOGL, META, MSFT).

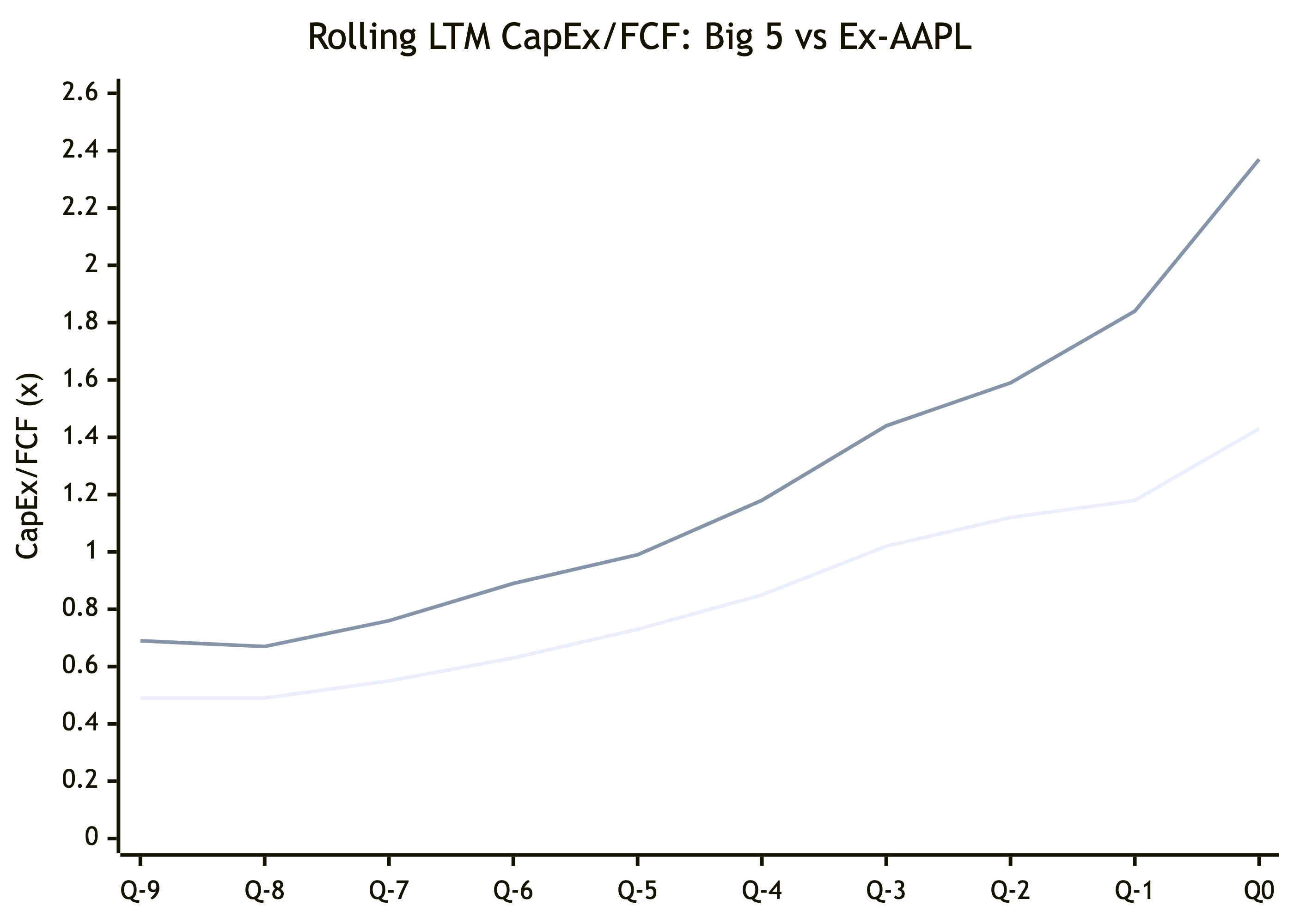

The Surprising Chart

I draw one conclusion: The group has not shown discipline yet.

CapEx pressure kept rising into the latest period. The climb steepens when I remove Apple.

Plain numbers:

- Big 5 went from 0.49x to 1.43x.

- Ex-AAPL went from 0.69x to 2.37x.

The trend shows an intensifying investment regime.

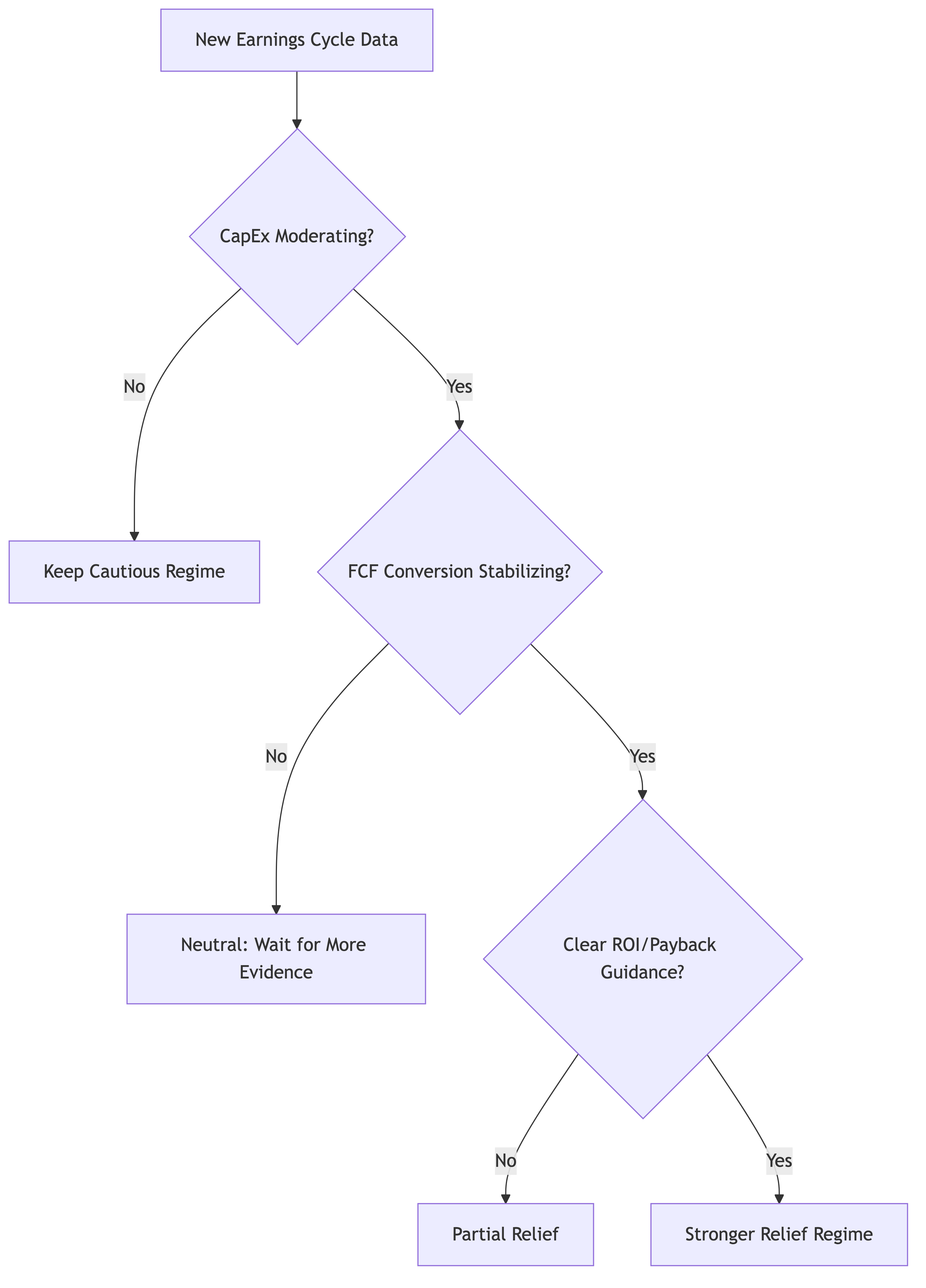

What Would Make Me Change My Mind?

I will change my view when numbers show discipline.

My current cases

To keep the framework explicit, I use three cases:

- Bull case (25%): monetization improves faster than expected, CapEx growth moderates, and FCF conversion strengthens.

- Base case (50%): pressure regime continues for now, evidence stays mixed, and discipline signals remain partial.

- Bear case (25%): CapEx stays elevated, FCF conversion weakens, and valuation pressure broadens.

Current base case: the group remains in a pressure regime, not yet in a discipline regime.

My checklist:

- At least two consecutive quarters of flat-to-down absolute CapEx in most core hyperscalers.

- Stable or improving FCF conversion while CapEx remains elevated.

- Guidance language shifts from "capacity expansion" to explicit ROI, utilisation, and payback thresholds.

Market reaction begins rewarding discipline consistently (not only rewarding bigger spend headlines).

If those four signals line up, I will move my base case from pressure regime to discipline regime and raise the bull-case probability.

What This Analysis Does Not Claim

To keep the scope clean, I do not claim four things:

- This analysis does not forecast stock prices.

- This analysis does not estimate intrinsic value.

- This analysis does not claim AI demand is weakening.

This analysis only tests one question: whether capital allocation behavior looks more disciplined over time.

Bottom Line

I asked one question: do AI leaders show better capital discipline?

The rolling panel says: not yet.

I treat this as a live process call. If those four conditions improve, I will update.